Let’s cut through the noise. The U.S. e-cigarette market is now a $9.1 billion giant, growing at 12.2% a year, and it’s still the single most important country for any vapor brand. By 2026, we’re looking at $10.2 billion, and by 2032, it could hit $18.2 billion. Globally, the U.S. takes up 23.4% of the $38.9 billion market. That’s massive. But the game has changed—new rules, new products, new headaches.

The Big Picture: Two Markets in One

Here’s something most reports don’t spell out clearly: the U.S. isn’t one e-cigarette market. It’s two.

- Legal channel (~40%): Mostly tobacco company brands like Vuse, NJOY, and a handful of PMTA-approved products. You’ll find these in convenience stores, but flavor choices are thin.

- Grey market (~54%): Dominated by Chinese brands—Geek Bar, Elf Bar, Lost Mary. No FDA authorization, but they’re everywhere. This is where the growth is.

- The rest (~10%): Smaller online brands, specialty devices, and emerging names.

This dual structure isn’t going away anytime soon. If you’re a brand or an investor, you need to decide which track you’re on.

Policy & Regulation: FDA + States – It’s Getting Tighter

The FDA keeps raising the bar. Since January 2026, all PMTA submissions have to go through a new electronic system. They’ve already sent out 700+ warning letters, mostly targeting unauthorized disposables and Chinese brands. But here’s the real twist: state-level rules are now often tougher than federal ones.

- Florida passed an “Age-Gate” law that restricts marketing of unapproved products.

- Kentucky now requires a special license to sell e-cigarettes.

- New York built a “legal product registry” – if it’s not listed, it’s illegal to sell.

So even if you somehow get past the FDA, you still have to navigate a patchwork of state rules. Retail licenses, product directories, flavor bans – it varies block by block.

And yes, the grey market is huge. Over half of the products sold don’t have FDA approval. Enforcement is stepping up – more customs seizures, more supply chain crackdowns – but the grey market adapts fast.

Product Trends: Disposables Still Rule, But They’re Getting Smarter

If you walk into any vape shop today, you’ll see the same thing: shelves packed with disposables. They make up 93% of products on the market and over 60% of dollar sales. The standard now is 15,000 to 30,000 puffs, USB-C charging, dual mesh coils, and – this is new – little digital screens showing battery life and puff count.

Flavors? That’s still the main event. Non-tobacco flavors grew 28.8%, and fruit flavors jumped 55%. Top sellers: Blue Razz, Watermelon Ice, Strawberry Ice, Mango. People buy disposables for the taste, period.

And the devices are starting to look like smartphones. Screens, power control, puff tracking. It’s not just a vape anymore – it’s a little piece of tech you carry around.

Brand Landscape: Who’s Actually Winning?

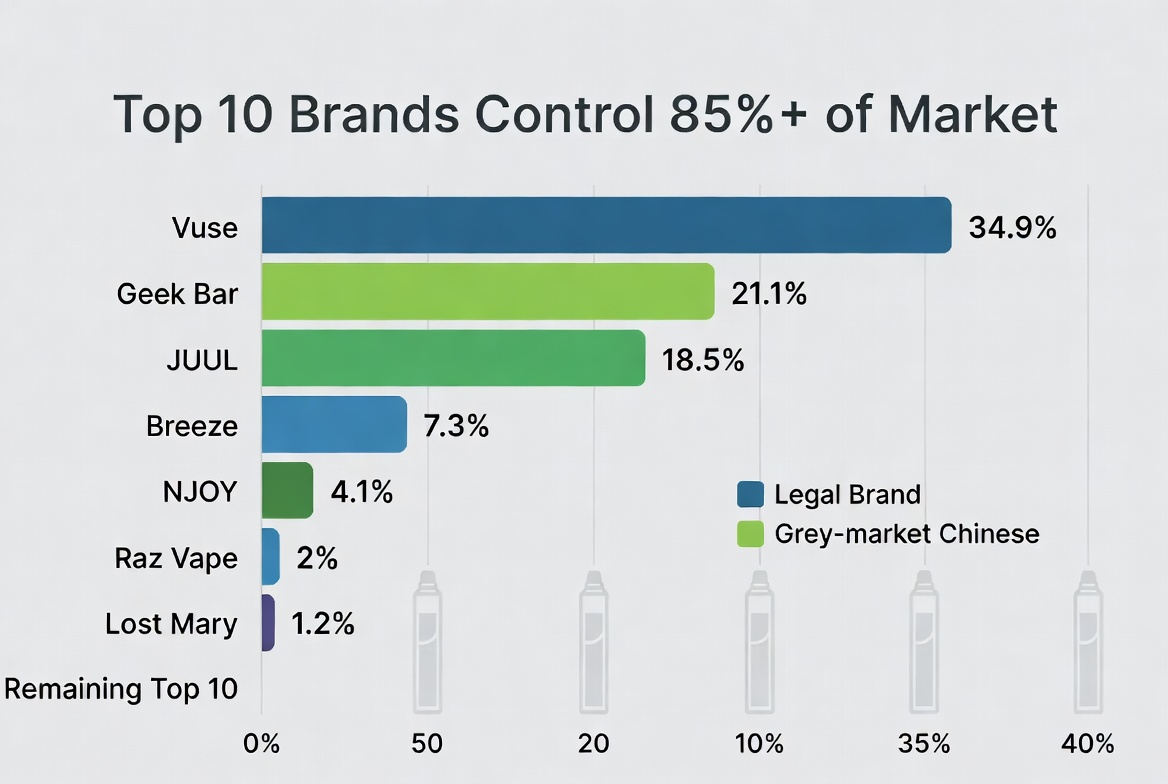

Let’s look at the numbers. Top 10 brands by market share:

- Vuse – 34.9%

- Geek Bar – 21.1%

- JUUL – 18.5%

- Breeze – 7.3%

- NJOY – 4.1%

- Raz Vape – 2%

- Lost Mary – 1.2%

- HQD – 1%

- Loon Maxx – 0.8%

- VAPEPIE– 0.5%

The top 5 control over 75% of the market. Top 10? Over 85%. But here’s the catch: about 70% of unit sales are unapproved products. That’s the grey market at work.

- Big Tobacco (Altria, BAT, PMI) own the legal channel with Vuse, NJOY, IQOS. They have PMTA approvals, so they sit comfortably in convenience stores.

- Legacy e-cig brands like JUUL and Logic are either approved or stuck in review. Their shelf space is shrinking.

- Chinese grey market brands – Geek Bar, Raz, Lost Mary – are the real growth stories. Geek Bar’s sales went up 729% in one year. Raz grew 232%. They’re fast, cheap, and aggressive.

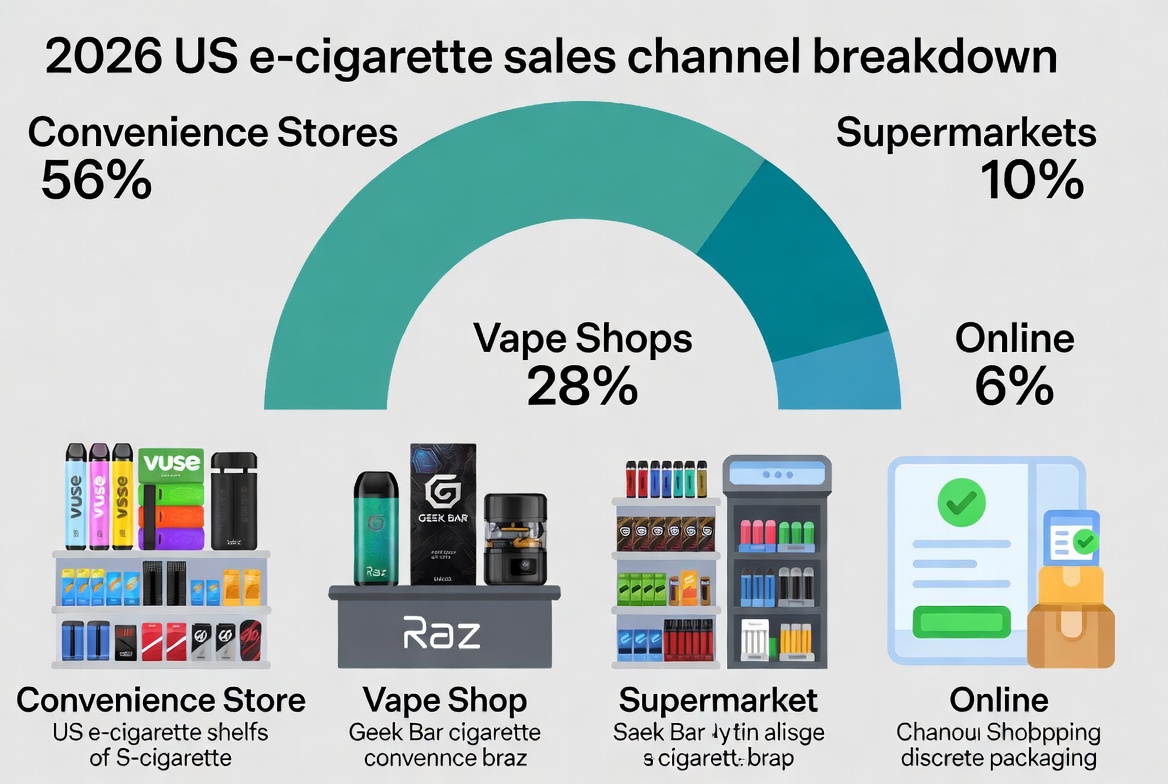

Where People Actually Buy (Channel Breakdown)

Convenience stores – 56% of all sales. 150,000+ stores across the U.S. But you can only sell what’s on each state’s approved list. Vuse owns 40% of C-store sales, JUUL 20%, Geek Bar/Lost Mary 12%, NJOY 6%. If you want volume, this is where you need to be – but you need the paperwork.

Vape shops – 28% of sales. About 8,000 specialty shops. This is where grey market brands thrive. Geek Bar Pulse, Raz LTX, refillable mods, exotic flavors. Higher ticket, loyal customers, less regulatory hassle (for now).

Supermarkets – 10%. Limited SKUs, heavy restrictions.

Online – 6%. Payment processors are a nightmare, but some brands still move units through discreet sites.

Who’s Vaping? The Consumer Story

-

67% male, 33% female – but women are catching up fast.

- Core age: 18 to 35. Young adults drive this market.

- Why do they vape? For many, it’s a cigarette alternative. But a huge chunk never smoked – they started with disposables because of the flavors and the buzz.

Also worth watching: nicotine pouches and heated tobacco. Pouches (like Zyn) are exploding – FDA has started approving more. Heated tobacco (IQOS) is slowly building. In a few years, e-cigarettes won’t be the only game in town. You’ll have three categories fighting for shelf space: vapes, pouches, and HNB.

The Chinese Brand Playbook: How They’re Winning

Geek Bar grew 729%. Raz grew 232%. Breeze grew 105%. How?

- Speed: They launch new products every few months.

- Big puffs + screens: 15k–30k puffs, LED displays, adjustable power.

- Flavor mastery: Blue Razz, Strawberry Ice, Mango – they know what sells.

Their strategy for entering the U.S.:

- Convenience stores: Small test runs, get state licenses, then scale.

- Vape shops: Build a brand story, train staff, offer higher-margin products.

- Online: Limited drops, influencer buzz, build scarcity.

Five Signals You Need to Watch in 2026

- No ban, but more barriers – The U.S. isn’t banning vapes. But they are licensing, listing, and limiting. Get used to paperwork.

- Grey market isn’t dying – 54% of products are still unapproved. Enforcement comes in waves, but the market adapts.

- Disposables dominate for years – At least 3–5 more years. 93% of products, 60%+ of sales. That’s not changing soon.

- Vapes are becoming gadgets – Screens, counters, Bluetooth? Maybe not yet, but they’re getting smarter.

- Three-way race coming – E-cigs, nicotine pouches, HNB. Don’t put all your money on one horse.

What Should Chinese Brands Do?

You’ve got three paths. None are easy, but each fits a different type of player.

Path one: Go legit (PMTA)

- Pros: Low long-term risk, brand equity, access to C-stores.

- Cons: Millions of dollars, years of waiting.

- Best for: Deep-pocketed companies thinking 5+ years ahead.

Path two: Ride the grey market

- Pros: Fast, low upfront cost, huge volume.

- Cons: Seizures, warning letters, state bans.

- Best for: Short-term players who can move quickly and absorb risk.

Path three: Out-innovate everyone

- Pros: You don’t need a famous brand – you need a better product.

- Cons: Copycats will follow within weeks.

- Best for: Teams that can design, manufacture, and ship new SKUs every 60 days.

The real winners will combine speed with smart channel strategy. Geek Bar didn’t win because of a brilliant logo. They won because they put a screen on a 20k-puff disposable, made it taste like Blue Razz, and got it into vape shops before anyone else.

Final Take

The US VAPE market is a tale of two worlds: legal and grey, slow and fast, boring and exciting. The barriers get higher every year – PMTA costs, state registries, retail licenses. But the opportunity is still massive. $10 billion by next year. 12% annual growth. And a user base that craves new flavors and smarter devices.

You just have to pick your lane. Then drive like hell.