Prepared for industry leaders and decision-makers looking at the German vape sector

Table of Contents

- Data Sources and Methodology

- Key Findings and Executive Summary

- Market Size and Growth Analysis

- Regulatory Environment and Policy

- Competitive Landscape and Brand Ecosystem

- Channel Structure and Distribution

- Consumer Behavior and Demand Structure

- Core City Structure

- Opportunities and Risk Assessment

- Top 10 German Distributors

- Nicotine Pouches and HNB Market

- 2026-2028 Trends and Final Decision

1. Data Sources and Methodology

We pulled this report together from the most reliable sources out there. The backbone comes from Statista and Euromonitor — the go-to names in global market research — plus official figures from the German Federal Statistical Office and EU-level compliance data through the Tobacco Products Directive (TPD) and the EU Common Entry Gate (CEG) system. We also drew on insights from Mordor Intelligence and ECigIntelligence, layered in direct channel checks and one-on-one conversations with players across the supply chain.

To keep things transparent, we used a dual-track approach:

- Official track: Strictly regulated, registered products based on government data.

- Industry estimate track: Adds in cross-border flows and any under-reported pieces, informed by real-world retailer and distributor feedback.

A few ground rules shaped everything: Germany runs a highly compliant market (gray-market share sits below 10%), taxation is the single biggest swing factor, and strong brand building plus airtight compliance are what separate winners from the rest. The numbers you’ll see lean heavily on the compliant side but already bake in a realistic view of the informal slice.

2. Key Findings and Executive Summary

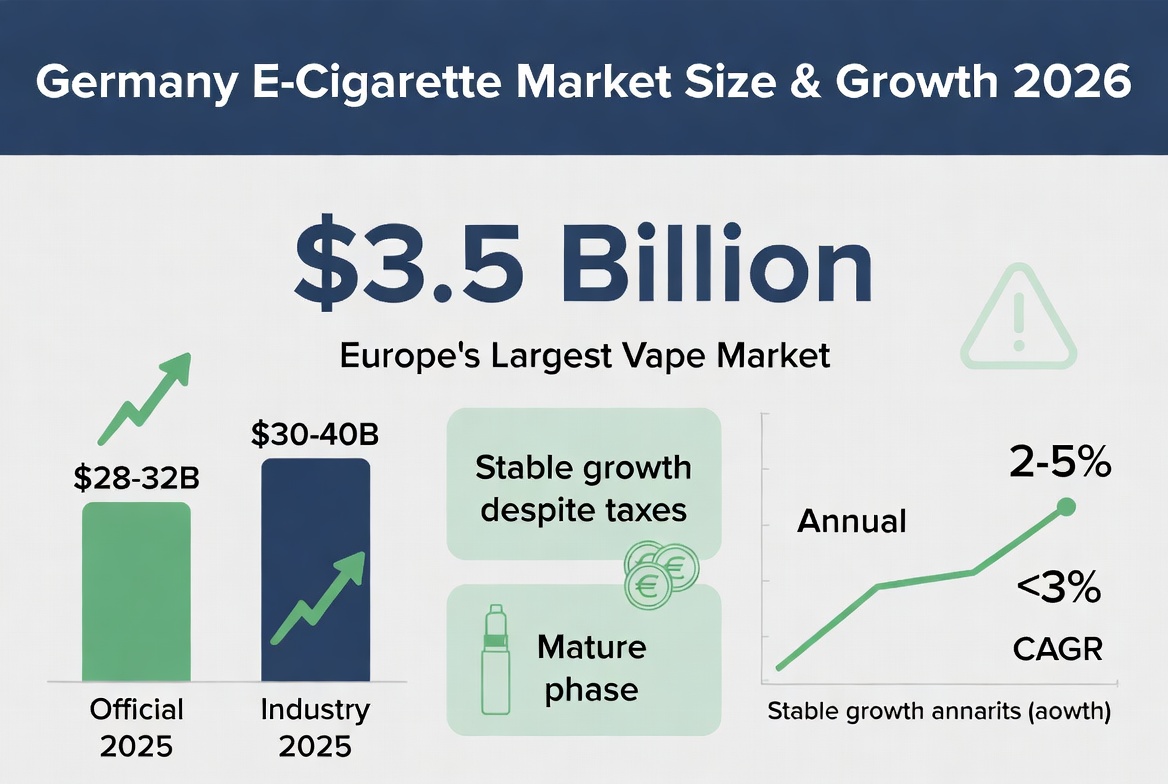

Germany is one of Europe’s biggest and most mature Vape markets — think high volume, high barriers, and a long game. We’re looking at a roughly $3.5 billion market in 2026, making it a standout on the continent.

The big picture

- Growth is steady but modest: 2–5% annually, with a CAGR around 3%. Taxes keep a lid on things, but the market isn’t shrinking.

- Disposable products are heading into tighter regulatory waters, while pod/refillable systems are gaining ground thanks to environmental pressure.

- The top three brands already control close to 60% of the market — concentration is real.

- Channels are dominated by big retail chains and specialist vape shops.

What this means for you

Enter if you’re in it for the long haul. Short-term flips won’t work here. Success comes down to three things that have to work together: strong branding, full regulatory compliance, and deep channel relationships. Risk sits at a medium level — the barriers are high, but once you’re in, they become your moat.

3. Market Size and Growth Analysis

By the end of 2025 the official numbers pointed to $28–32 billion, while industry estimates (including some gray flows) landed between $30–40 billion. We settled on $3.5 billion as the realistic 2026 figure. Expect it to land between $3.5–3.8 billion next year.

Growth has settled into a stable 2–5% range. That’s not explosive, but it’s resilient. The compound annual growth rate sits around 3%. Germany remains Europe’s largest single Vape market, but policy (especially taxes) is the main brake.

Product mix today

- Open systems: 15%

- Pod/refillable: 35%

- Disposables: 45%

- Other: 5%

The tax effect

Liquid tax runs $0.25–0.30 per ml. That hits both nicotine and nicotine-free products and is the single biggest drag on volume. Still, the underlying driver — smokers looking for better alternatives — keeps the market moving forward. We’re seeing a clear shift from disposables toward pods as environmental rules tighten.

4. Regulatory Environment and Policy

Germany is one of the strictest regulated vape markets in Europe, and that’s not changing anytime soon.

Current framework (fully TPD-compliant)

- Max nicotine strength: 20 mg/ml

- Max tank/pod volume: 2 ml

- Mandatory EU-CEG notification for every product

Recent and upcoming moves

- Stronger focus on disposable regulation and environmental impact (battery recycling, traceability).

- Ongoing youth-protection rules: flavor and marketing restrictions keep getting tighter.

The tax story

Germany is one of the few EU countries with a dedicated e-liquid excise tax that covers both nicotine and zero-nic liquids. It’s applied by volume and keeps rising. The system is stable in structure but keeps tightening on the edges — expect higher compliance costs and higher barriers for anyone new to the market.

Bottom line: the rulebook is basically written. Short-term shocks are unlikely, but steady pressure on taxes, environment, and youth access will continue.

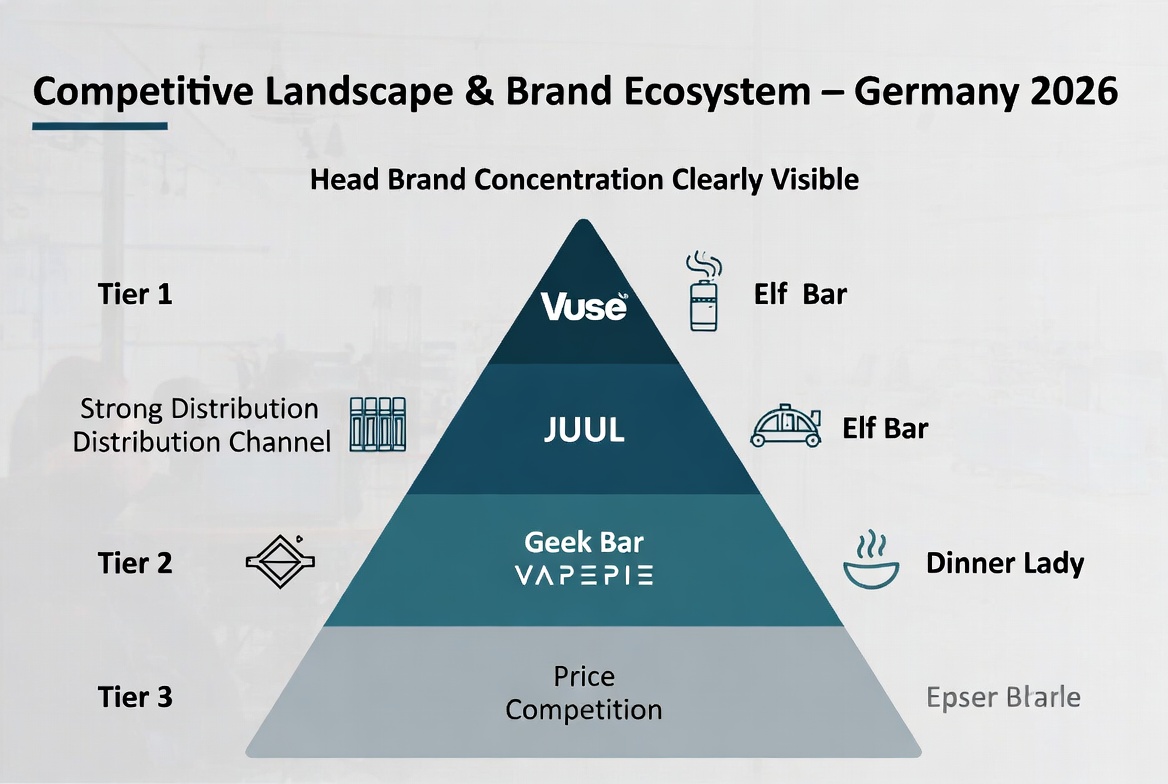

5. Competitive Landscape and Brand Ecosystem

The market is clearly tiered and getting more concentrated.

Tier 1 (the leaders) – CR3 close to 60%

Vuse, JUUL, Elf Bar. These brands own broad distribution, high awareness, and strong retailer loyalty.

Tier 2 (fast climbers)

Geek Bar, VAPEPIE, Dinner Lady. They’re growing by nailing channel partnerships and moving quickly.

Tier 3 (the rest)

Smaller brands fighting mainly on price. Shelf space is getting harder to hold.

New entrants face real hurdles. Brand recognition and compliance muscle are now table stakes. The days of easy distribution for unknowns are over.

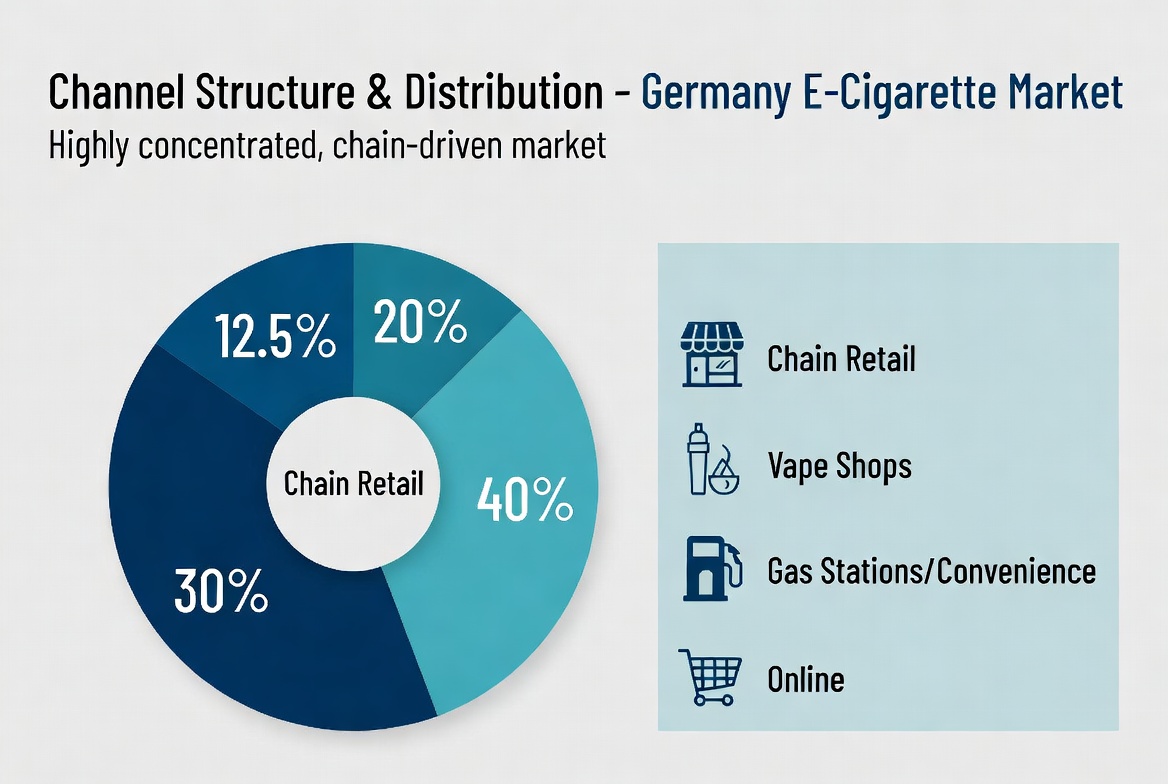

6. Channel Structure and Distribution

Distribution is professional, concentrated, and increasingly chain-driven.

Channel split

- Chain retail: 40%

- Vape specialist shops: 30%

- Gas stations / convenience: 20%

- Online: 12.5%

The big chains set the tone — standardized processes, scale advantages, and high entry requirements. Brands that want prime placement need proven credentials and long-term commitment. The shift from pure wholesale push to chain-terminal pull is well underway and still accelerating.

7. Consumer Behavior and Demand Structure

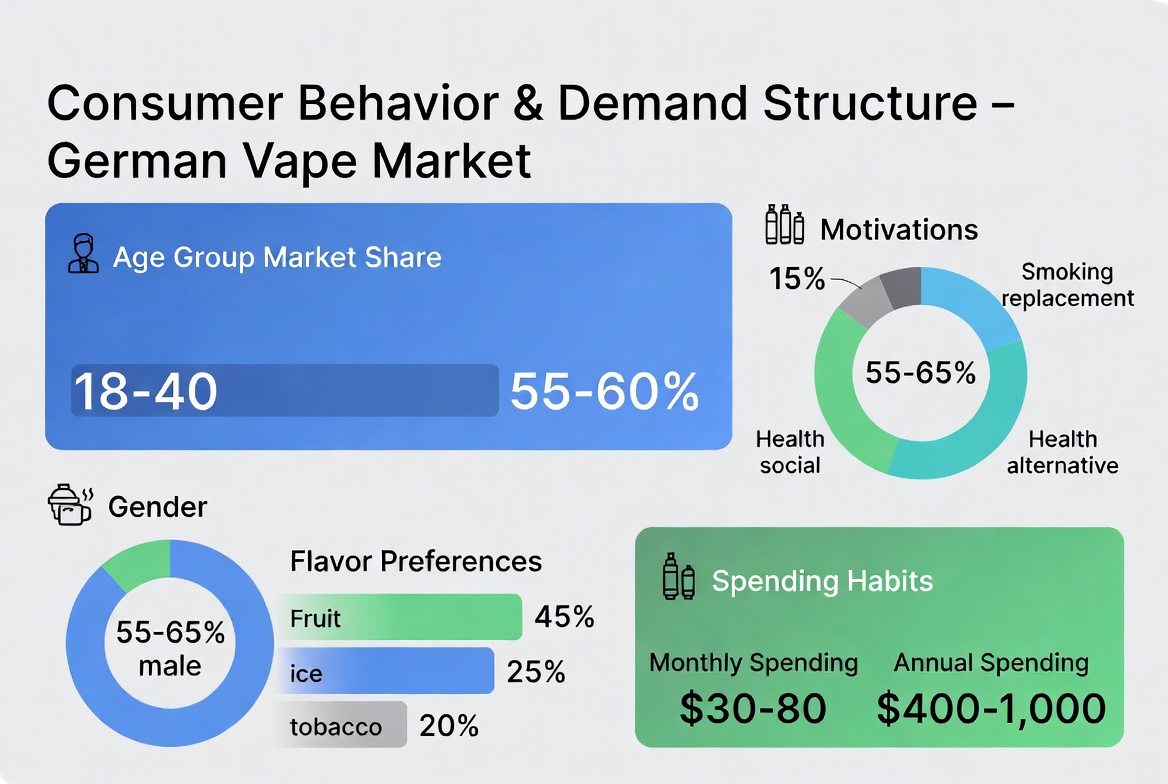

Who’s vaping

- Age: 60% are 18–40

- Gender: 55–65% male

- Nicotine preference: 10–20 mg/ml is the sweet spot

Why they vape

- Smoking replacement: 55%

- Health-conscious alternative: 25%

- Social / lifestyle: 15%

- Other: 5%

Flavor breakdown

- Fruit: 45%

- Ice/cooling: 25%

- Tobacco: 20%

- Dessert/other: 10%

Fruit and ice together dominate (70%+). German consumers have solid spending power — average monthly spend $30–80, annual $400–1,000. That’s noticeably higher than in southern Europe and gives brands room to build real premium positioning.

8. Core City Structure

Consumption is heavily concentrated in the economically strong urban centers.

Tier 1 cities (Berlin, Hamburg, Munich): ~45% of the market

Tier 2 (Cologne, Frankfurt): ~30%

Tier 3 (Düsseldorf and others): ~25%

If you’re building presence, these top cities are where the volume and the trendsetters live.

9. Opportunities and Risk Assessment

Biggest opportunities

- High unit value: * German vapes spend more per user than in most of Europe.

- Brand equity: Once you win trust, loyalty sticks.

- Pod systems: The move away from disposables (driven by regulation and eco-rules) creates clear runway.

- Nicotine pouches: The fastest-growing new category (15–25% annual growth) and still early.

Key risks

- Rising taxes squeezing margins and consumer prices.

- High compliance costs (testing, registration, ongoing updates).

- Channel access — the top doors are not wide open without strong credentials.

- Potential further restrictions on disposables.

Overall profile: High-scale market + high barriers + medium risk. Built for patient, well-resourced players. Short-term arbitrage is not the play.

10. Top 10 German Distributors

The market is controlled by a mix of large distributors and strong retail chains.

Tier 1 – Market shapers

- InnoCigs: One of the biggest national distributors and a true market gateway.

- Riccardo: Major chain operation with strong physical retail footprint.

- Dampfdorado: Strong online-offline hybrid with serious e-commerce muscle.

- InTrade: Broad multi-brand distribution and wide geographic reach.

- KLS: Excellent supply-chain and logistics capabilities.

Tier 2 – Regional and specialist

- Liquidwerk (specialist e-liquid channel)

- Avoria (local brand + distribution)

- Ultrabio Werke (local manufacturing strength)

- Lynden (premium/high-end focus)

Tier 3 – E-commerce and niche

- Zazo, HighendSmoke and other online-focused players.

Takeaway: Success in Germany is a partnership game between distributors and chain retailers. You need both.

11. Nicotine Pouches and HNB Market

Nicotine pouches

This is the breakout category. Current size $300–500 million, growing 15–25% a year. It’s the fastest-expanding segment and still relatively open for smart entrants.

Heat-not-burn (HNB)

Roughly $1.0–1.5 billion. IQOS dominates, with very high user loyalty and repeat purchase rates. The market is effectively locked down by the big tobacco players — entry is tough unless you bring something truly differentiated.

Strategic view: Vapes remain competitive and open; HNB is largely closed; pouches are the real growth story worth prioritizing.

12. 2026-2028 Trends and Final Decision

What’s coming

- Steady 2–4% overall growth as the market matures.

- Continued brand concentration (CR3 likely to rise).

- Rising compliance and tax pressure.

- Multi-category competition: Vapes, pouches, and HNB all fighting for share of the “reduced-risk” wallet.

Three-phase entry plan for serious players

Phase 1 (0–6 months): Test the waters in 2–3 strong Tier-2 cities and secure initial distributor partnerships.

Phase 2 (6–18 months): Invest in brand visibility and consumer education.

Phase 3 (18+ months): Move into the major chain systems with proven traction.

Final call

Germany is a high-scale, high-barrier, medium-risk mature market. It rewards long-term commitment and punishes shortcuts. If you can bring real brand strength, full compliance, and genuine channel partnerships, the opportunity is substantial. For the right player it’s a “yes” — but only if you’re built for the long game.