Executive Summary: Key Takeaways

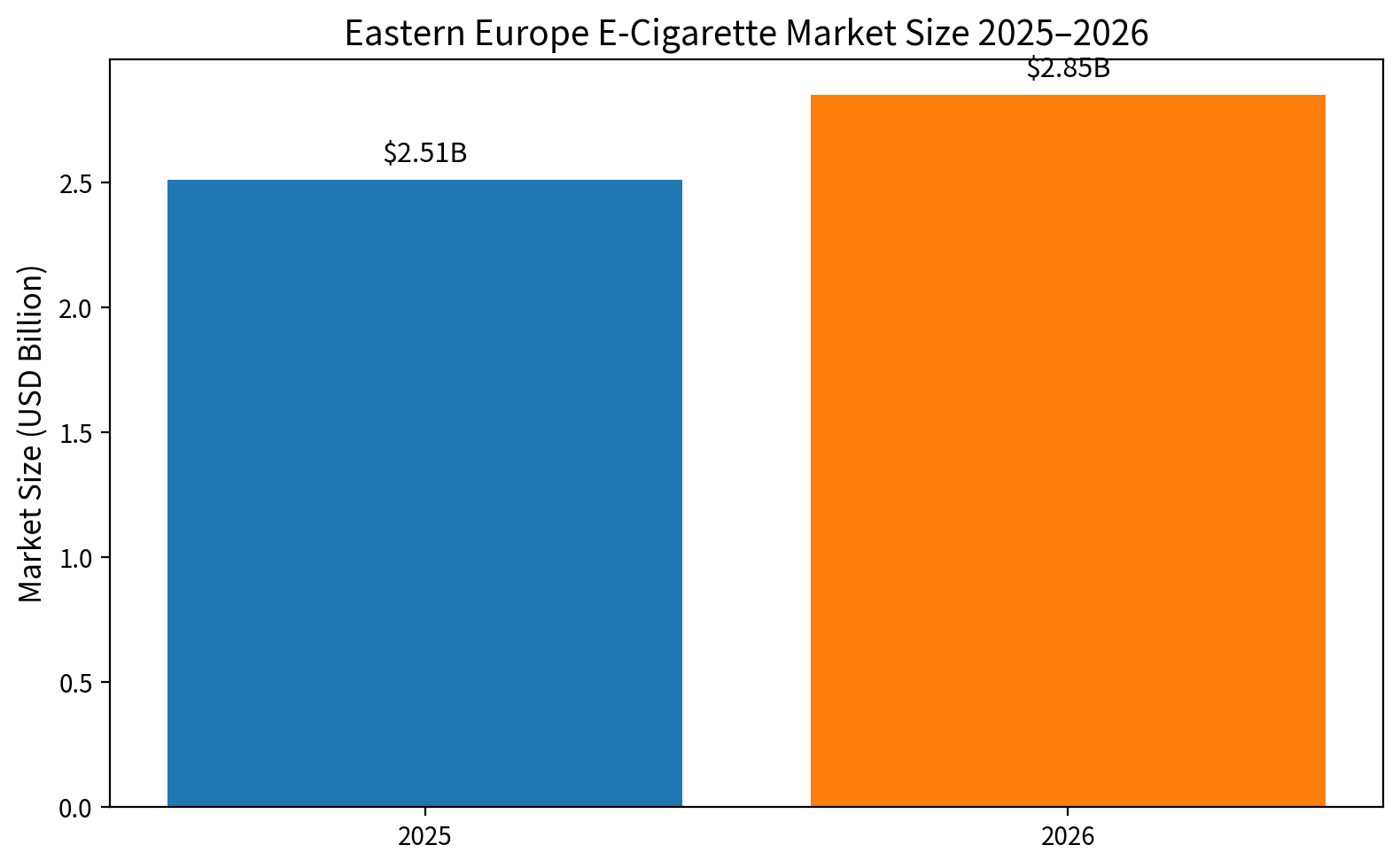

The Eastern European e-cigarette (vape) market continues to show strong momentum heading into 2026. Our latest projections put the total regional market size at approximately $2.5 billion in 2025, rising to $2.85 billion in 2026 (with a realistic range of $2.2–3.5 billion when including grey-market flows).

Growth remains robust — CAGR of 10%+ through 2028 — making Eastern Europe one of the fastest-expanding vape regions in Europe, outpacing Western markets. Disposable vapes still dominate at 65%+ of sales, though the window for easy gains is narrowing.

Core drivers:

- Large base of traditional smokers shifting to vaping

- Strong price sensitivity met by competitive Chinese supply chains

- Fragmented distribution that rewards fast-moving players

Biggest watch-out: Policy uncertainty varies sharply by country and can change quickly. Brands that move early, lock in strong local distributors, and keep a close eye on regulation will capture the biggest upside.

Market Size & Growth Trends (2025–2026)

| Year | Market Size (USD) | YoY Growth |

|---|---|---|

| 2025 | ~$2.51 billion | - |

| 2026 (proj) | ~$2.85 billion | +13–15% |

What’s powering the growth

- Penetration gap: Vaping adoption in Eastern Europe still lags Western Europe by 30–50%. Millions of adult smokers represent a massive conversion opportunity.

- Affordability edge: Chinese manufacturers deliver high-quality, high-nicotine products at prices local consumers love.

- Channel momentum: National and regional wholesalers are rapidly expanding shelf space across convenience stores, kiosks, and vape shops.

Headwinds to watch

Tightening taxes and regulatory shifts could slow momentum. Even so, the overall outlook stays positive for players who plan for volatility rather than hoping it disappears.

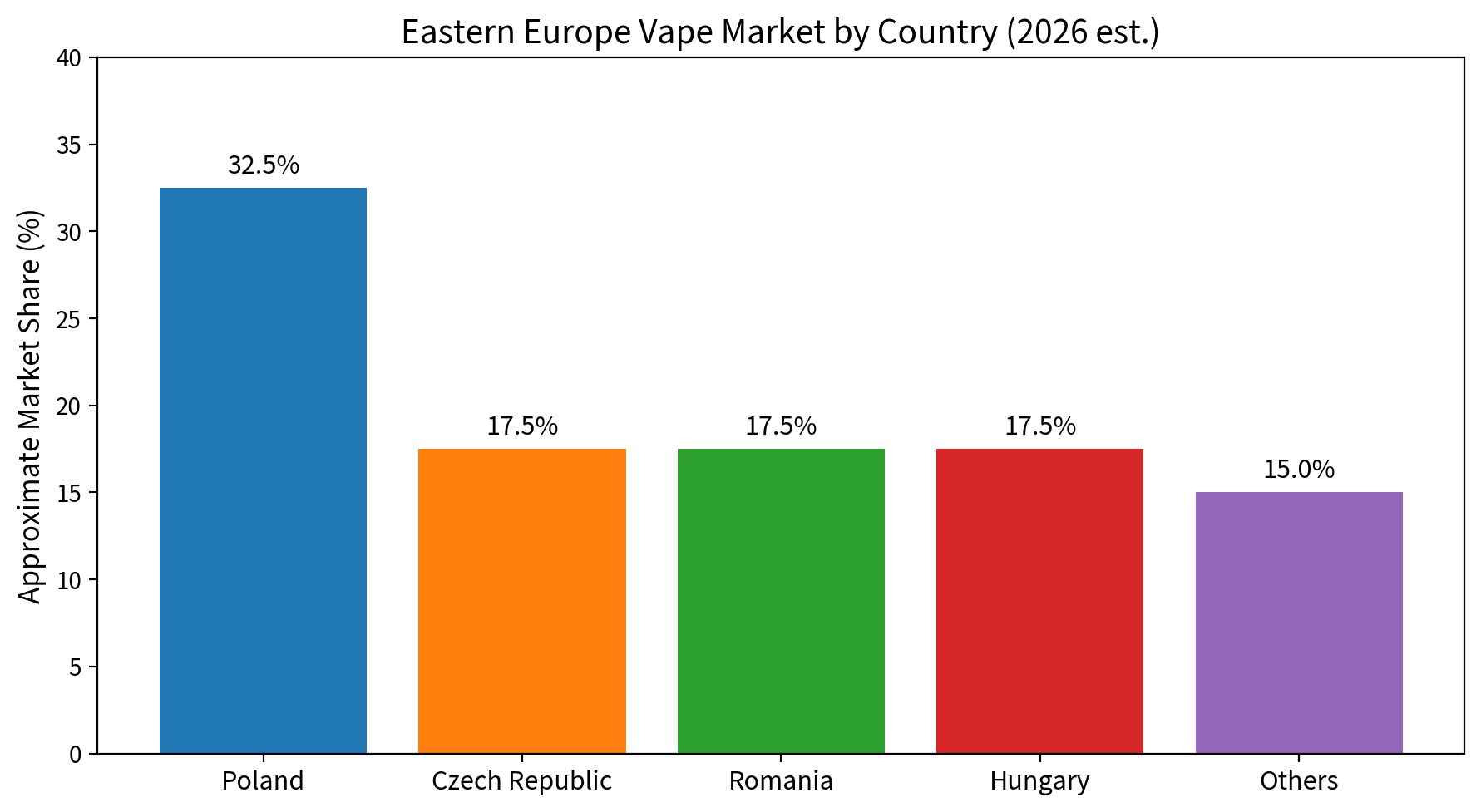

Country Market Structure

Tier 1 (≈50% of regional volume)

- Poland: 30–35% share — the undisputed heavyweight and most mature market. Must-win territory.

- Czech Republic: 15–20% share — higher spending power and relatively relaxed rules.

Tier 2 (≈30%)

- Romania: 15–20% — fastest-growing, very distributor-driven.

- Hungary: 15–20% — more regulated, slower but stable once you’re in.

Tier 3 (≈20%)

Slovakia, Bulgaria, and smaller neighbors — worth opportunistic expansion once the core markets are solid.

Poland remains the anchor: Any serious Eastern Europe strategy starts here.

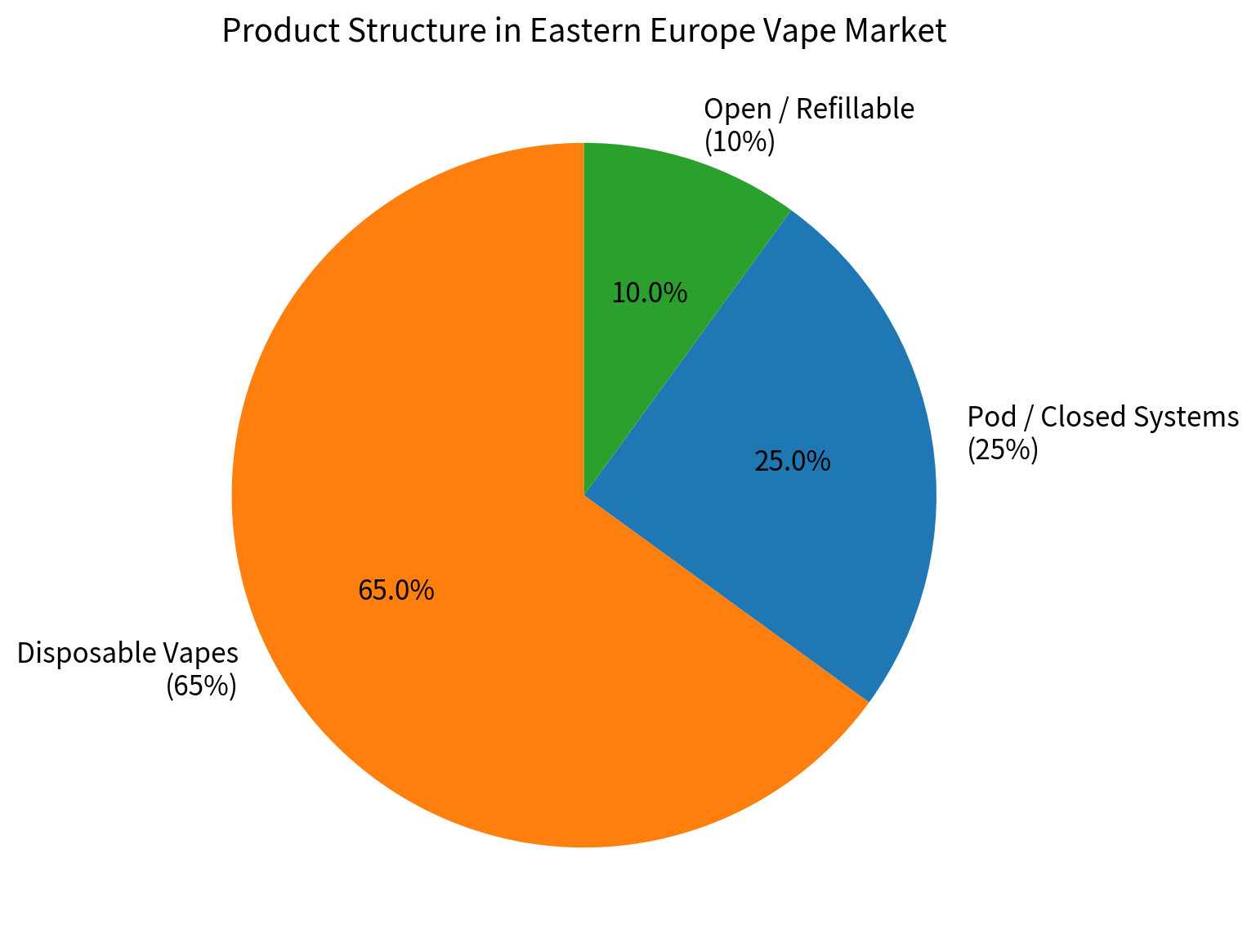

Product Structure & Consumer Preferences

Device breakdown

- Disposable vapes: 65% — still the clear leader

- Pod/closed systems: 25%

- Open-system / refillable: 10%

Flavor preferences

- Fruit: 55%

- Ice/menthol: 25%

- Tobacco: 12.5%

- Other: 5%

Typical user profile

- Age: predominantly 18–35

- Annual spend: $200–600

- Price-sensitive but open to quality upgrades and strong nicotine options

Key insight: Disposable products are still in their sweet spot, but that window is shortening. Smart brands are already preparing hybrid portfolios for the next phase.

Competitive Landscape & Brand Ecosystem

Tier 1 (40–50% combined share)

- Elf Bar

- Lost Mary

- Geek Bar

Tier 2 (30–40%)

Strong regional players and new entrants leveraging aggressive pricing and flavor innovation.

Tier 3 (20%)

Local micro-brands that survive mainly on price and hyper-local relationships.

Overall picture: Concentration is lower than in Western Europe, leaving room for new entrants. Chinese-origin brands still lead, but success depends more on distribution muscle than pure brand equity.

Channel Structure & Distribution Reality

Wholesale/Agency dominance

- Wholesalers & agents: 55% of volume — the real gatekeepers

- Vape shops: 25–30% — best for brand building

- Convenience stores / kiosks: 35% of retail sales — the true volume engine

- General retail: 15–20%

- Online: 15% (higher in Czech Republic)

Practical takeaway: The fastest route to scale is securing 2–3 strong national or regional distributors. Vape shops build image, but smoke shops, kiosks, and convenience stores deliver the actual volume.

In-Depth Country Snapshots

Poland

Largest and most developed market. National distributors plus strong regional wholesalers. Taxes are higher and regulation is tightening, but the infrastructure is mature. Priority move: Partner with top-tier agents early.

Romania

High-growth, distributor-led market. Fast rollout possible, but policy swings and channel instability require tight risk management. Ideal for aggressive volume plays.

Czech Republic

Higher disposable income, more relaxed policy environment, and stronger online penetration. Smaller, more fragmented agents dominate — perfect for a multi-distributor, test-and-learn approach.

Hungary

Heaviest government oversight and restricted private channels. National regulatory gatekeepers control much of the flow. Approach with caution — best left for later-stage diversification.

Market Opportunities (Top 5)

- Smoker conversion window — huge untapped adult smoker base with low switching friction.

- Low channel barriers — no single player owns the market; speed beats perfection.

- Disposable product tailwind — 60–70% share and low consumer barriers still driving easy volume.

- Price elasticity — Chinese supply-chain cost advantages match perfectly with local price sensitivity.

- Multi-country parallel rollout — one strong agent network can open several doors at once.

Market Risks (Top 5)

- Policy shock — sudden bans or tax hikes on disposables (highest severity).

- Grey-market pressure — 20–40% of volume undercuts legitimate pricing.

- Price wars — low brand loyalty and product similarity can crush margins quickly.

- Distributor volatility — relationship-driven markets mean agents can switch or run credit risks.

- Regulatory fragmentation — every country moves at its own pace.

Risk-Reward Profile

High growth × high volatility. The region rewards early movers who combine speed with disciplined risk controls.

Strategic Recommendations & Final Verdict

Should you enter? Yes — and the sooner the better. The window is still wide open in 2026, but it will not stay that way forever.

Three-phase entry playbook

Phase 1 (0–3 months): Secure 2–3 high-quality distributors in Poland and Czech Republic. Build the initial network fast.

Phase 2 (3–9 months): Multi-SKU rollout, aggressive shelf-space push, volume acceleration.

Phase 3 (12+ months): Stabilize pricing, professionalize distributor relationships, and start building real brand equity.

Risk-control must-haves

- Keep inventory turns inside 3 months

- Spread exposure across 3–4 countries

- Monitor policy signals weekly

Bottom line: In Eastern Europe’s vape market, success isn’t about being the best — it’s about being early. The brands and distributors who act decisively in 2026 will set the competitive table for the rest of the decade.

Ready to move? The data is clear: the opportunity is real, the risks are manageable, and the clock is ticking.